Life settlements, often misunderstood and overlooked, are integral to understanding the landscape of financial planning. They offer a unique way for policyholders to maximize the value of their life insurance policies.

This article will delve into what life settlements are, compare them with viatical settlements, explore key terminologies, and trace their historical roots. Read on for all the details.

Defining Life Settlements: A Top Life Settlement Company Perspective

Life settlement, as defined by top life settlement companies, is a strategic financial transaction involving the sale of an existing life insurance policy. The policyholder sells their policy to a 3rd party, often a top life settlement company. This transaction is facilitated for a one-time cash payment that exceeds the policy’s cash surrender value but falls short of its net death benefit.

Future premiums are paid by a top life settlement company. This process allows the policyholder to receive immediate cash for a policy they no longer need or can afford, often significantly more than what they would receive if they surrendered the policy to the insurance company.

By engaging with a top life settlement company like Abacus Life Settlements, policyholders can ensure they maximize the potential financial benefits from their life insurance policies. It’s important to note that not all policies qualify for a life settlement. The insured should typically be at least 65 years old, and the policy should have a minimum death benefit of $100,000. Often purchased policies include universal Life, convertible term, whole Life, and second-to-die policies.

A life settlement can be valuable if you consider letting your policy lapse or surrendering it to the insurance company. By working with a top life settlement company, you can often secure a higher payout and make a financially beneficial decision.

Life Settlement Terminology

Understanding life settlements requires familiarizing yourself with some key terminologies. Here are the main ones:

- Beneficiary: The beneficiary is a person or entity you designate to receive the death benefit of your life insurance policy upon death. Beneficiaries can be individuals, trusts, charities, or businesses. This transition of roles signifies the transfer of rights and responsibilities, ensuring a seamless continuation of the policy’s terms and conditions.

- Cash Surrender Value: This is the sum of money the insurance company will give the policyholder if they choose to end the policy early or if the insured person passes away. It’s essentially the savings component of a whole life insurance policy. Life settlement transactions typically result in a selling price that exceeds the cash surrender value.

- Convertible Term Life Insurance: This feature provides flexibility and ease in transitioning to a long-term coverage option, ensuring peace of mind for the policyholder. This conversion can be a valuable feature if the policyholder’s health deteriorates and they still want life insurance coverage.

- Death Benefit: This is what an insurance company pays to a beneficiary(s) after the insured person’s death. The death benefit is tax-free under current law and determined at the policy’s inception. In a life settlement transaction, the buyer eventually collects the death benefit.

- Face Value: This is the original death benefit amount stated in the life insurance policy. It’s the amount the policy is supposed to pay upon the insured’s death, not including any additional amounts added by policy growth or subtracted by loans or withdrawals.

- Illustration: An illustration in life insurance is a document that shows the policy’s projected future values, including death benefits and cash surrender values. It’s based on various assumptions and is often used to help policyholders understand how their policy might perform over time.

- In-force: A policy is considered “in-force” when all premiums are up-to-date, and the policy is active and will pay out according to its terms. If a policyholder stops paying premiums, the policy may lapse and become void.

- Lapse: When a policyholder stops paying premiums, the life insurance policy may lapse or terminate. Once a policy lapses, the insurance company can no longer pay the death benefit.

- Term Life Insurance: This type covers a specific period or “term” (like ten, twenty, or thirty years). Term life policies do not build cash value and typically offer lower premiums than permanent life insurance.

- Whole Life Insurance & Universal Life Insurance: Permanent life insurance covers the insured person for their entire life. Whole Life insurance has stable premiums and a guaranteed cash value, and universal life insurance has adjustable premiums as well as a cash value that can change with interest rates. Both types of insurance can be sold in a life settlement transaction.

Comparison: Life Settlements Vs. Viatical Settlements

Although similar, Life and viatical settlements cater to different demographics and circumstances. Life settlements primarily target senior policyholders over 65 who are in good health but no longer need or can afford their life insurance policies. By selling their policy, they unlock more value with the buyer assuming all future premium payments.

On the other hand, viatical settlements cater to policyholders who are either terminally or chronically ill, regardless of age, and have a life expectancy of less than two years. Here, the policyholder sells their policy for an immediate cash payment, typically higher than a life settlement due to the shorter life expectancy. The buyer pays all future premiums and becomes the sole beneficiary. Thus, while both involve selling a life insurance policy, they vary based on the insured’s health status and life expectancy.

History of Life Settlements

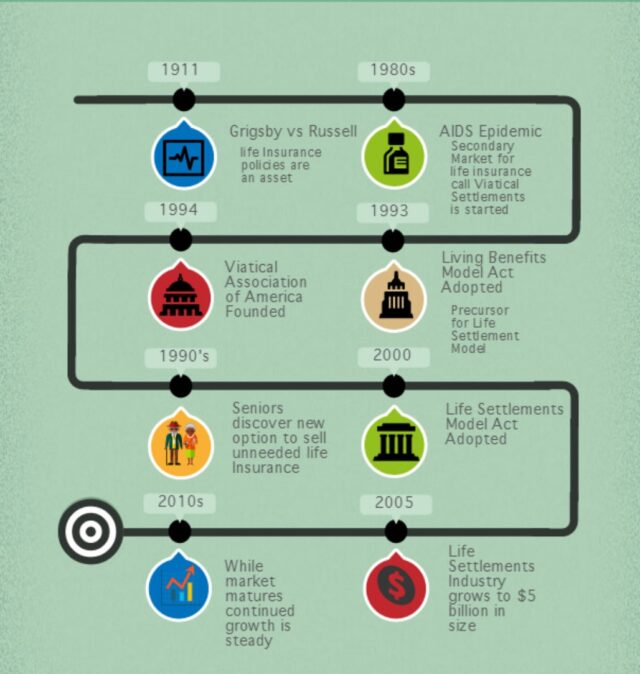

The concept of life settlements isn’t new. Its roots date back to 1911 when the United States Supreme Court ruled in Grigsby v. Russell that life insurance policies are personal property that could be sold at the owner’s discretion.

However, it wasn’t until the late 1980s that life settlements, in the form of viatical settlements, became more prominent. These were primarily offered to individuals facing life-threatening illnesses like cancer or HIV/AIDS. The industry has since evolved into a well-regulated space with state licensing requirements.

Unraveling the Power Of A Top Life Settlement Company

A Top Life Settlement Company offers a viable solution for policyholders to extract maximum value from their life insurance policies. Understanding this can open up new avenues for financial planning.

While a top life settlement company may not suit everyone, knowing what they can do empowers you to make informed decisions about your financial future. As the saying goes, knowledge is power, and in the case of life settlements, it could also mean more money in your pocket.